Cash flow is what separates a business that can make payroll, invest, and absorb a slow month from one that can't, even when the books say it's profitable.

Most finance leaders don't struggle because they lack revenue. They struggle because the cash arrives later than the bills do. That gap, between the work you deliver and the money that actually lands in your account, is where the pressure builds.

When teams ask how to improve cash flow, the honest answer is that it's rarely one fix. It's a set of habits that tighten the cycle from sale to settlement.

This guide covers what cash flow really is, why it stalls, and the practical steps you can take, with a focus on the lever most finance teams control directly: getting paid faster.

What is cash flow?

When more comes in than goes out, you have positive cash flow. When the reverse is true, cash flow is negative, and you're drawing down reserves to keep operating.

Cash flow is about timing: when the money actually shows up. A company can be profitable on paper and still run out of cash if customers pay slowly and obligations come due first. This is why solvency is measured in days, while profitability is measured in quarters.

Cash flow answers "how much money actually moved in and out of the bank?" This is the only one that tracks real dollars hitting or leaving the account, when they hit or leave. It ignores what you've "earned" or "owe" on paper and just follows the money.

Revenue answers "how much did we earn?" It's the value of what you sold in a period, recorded when you earn it — not necessarily when cash arrives. If you sign a customer to a £12k annual contract, you've earned £1k of revenue each month as you deliver the service, regardless of when they pay. Revenue is a promise being fulfilled, booked on the income statement.

Profit answers "did we earn more than we spent?" It's revenue minus expenses over the same period. Also accrual-based — expenses get matched to the period they belong to, not when you paid them. Profit is still a paper concept: you can be profitable on the income statement and have no money in the bank.

The 3 types of cash flow

Financial statements break cash flow into three categories:

- Operating cash flow: the cash generated by your core business activities, such as selling products or services and collecting on invoices

- Investing cash flow: cash tied to buying or selling assets, like equipment or investments

- Financing cash flow: cash from raising capital, taking on debt, or returning money to owners and investors

For most operating businesses, the first category is where day-to-day health lives. Learning how to improve cash flow from operations means shortening the time between delivering value and collecting payment, because that's the cash you can rely on without borrowing or selling assets.

The cash conversion cycle

The cash conversion cycle measures how long it takes to turn the money you spend on delivering a product or service back into cash in the bank. The longer that cycle, the more working capital gets trapped in unpaid invoices and inventory.

For B2B companies, the biggest driver of a long cycle is usually Days Sales Outstanding (DSO): the average number of days it takes to collect after a sale.

Strong accounts receivable management is the most direct way to compress that number.

Why cash flow problems happen

Before you can fix cash flow, it helps to understand where it leaks. Knowing how to improve cash flow problems starts with diagnosing the cause, because the right fix for slow collections is different from the right fix for lumpy revenue.

Late payment is the most common culprit. The Atradius Payment Practices Barometer found that 44% of B2B credit sales in North America were overdue in 2025. When nearly half of what you're owed arrives late, your cash position becomes hard to predict no matter how healthy the underlying business is.

The cost is real. A 2025 survey from The Kaplan Group found that 93% of companies report revenue loss from late payments, and in fast-scaling sectors like SaaS, 22.2% lose more than 10% of annual revenue.

Separately, Allianz Trade reported that global DSO rose by two days in its latest review, meaning many companies are effectively acting as informal lenders to their customers.

• You're consistently waiting on a large share of invoices past their due date

• DSO is climbing, or you don't measure it at all

• Revenue is lumpy and hard to forecast more than 30 days out

• Collections rely on someone manually sending the same reminder emails

• You lack a clear, real-time view of what you're owed and when it's expected

How to improve cash flow: 8 practical steps

Whether you're working out how to improve cash flow in a business with ten customers or how to improve company cash flow across hundreds of accounts, the levers are similar.

The steps below move roughly from quickest to implement to most structural.

- Invoice faster and more accurately. The clock on every payment starts when the invoice goes out, not when the work is done. Send invoices the moment a milestone or billing period closes, and make sure the amount, terms, and line items are correct so disputes don't stall payment. Clean B2B billing is the foundation everything else rests on.

- Set clear credit terms and policies. Decide who gets credit, how much, and on what terms before you sell, not after an invoice goes unpaid. Tighter terms (net-15 or net-30 instead of net-60) pull cash forward, and consistent enforcement signals that you take payment seriously.

- Automate collections and follow-ups. Manual chasing is slow, inconsistent, and easy to deprioritize. Automated reminders sent on a defined cadence, sometimes called dunning, keep every overdue invoice moving without anyone copying and pasting the same email. This is one of the highest-leverage moves for how to improve a business cash flow.

- Offer multiple, frictionless payment methods. Every extra step between an invoice and a payment is a chance for delay. Supporting ACH, wire, cards, and digital wallets, and letting customers pay in their preferred currency, removes excuses and shortens settlement time.

- Prioritize at-risk accounts to reduce DSO. Not every overdue invoice deserves the same attention. Score accounts by likelihood of late payment and focus your team's energy on the ones that matter most. Targeted outreach is the practical path to reduce DSO without simply working harder.

- Reconcile and apply cash quickly. Cash that's received but not matched to an invoice is cash you can't confidently act on. Fast, accurate cash application closes the loop so your records reflect reality and your team stops chasing payments that already arrived.

- Manage the outflow side too. Improving cash flow isn't only about collecting faster. Negotiate sensible terms with your own suppliers, time large outflows around expected inflows, and review recurring costs regularly. The goal is to keep more cash in the business for longer without damaging supplier relationships.

- Build a rolling cash flow forecast. A 13-week forecast turns weekly inflows and outflows into a visibility window that flags a gap before payroll lands. Forecasting is how you move from reacting to cash crunches to anticipating them, and it's central to figuring out how to improve cash flow of a business over the long term.

None of these steps requires a complete overhaul. Even picking two or three is a workable answer to how to improve cash flow in a company that's feeling the squeeze. For a deeper treatment of the collections side specifically, see our guide on how to improve your accounts receivable.

5 common cash flow problems and how to address them

Best practices for cash flow management

The steps above fix specific leaks. The practices below are about how to improve cash flow management as an ongoing discipline rather than a fire drill. They're what separate teams that occasionally catch up from teams that stay ahead.

- Measure what matters. Track DSO, the cash conversion cycle, and cash buffer days consistently. You can't manage a number you don't watch.

- Make cash flow visibility real-time. Knowing how to improve cash flow visibility usually comes down to replacing month-end spreadsheets with a live view of what's owed, what's overdue, and what's at risk.

- Standardize your collections cadence. A documented sequence of reminders and escalations means nothing falls through the cracks when someone is on vacation.

- Segment customers by risk. Treat a reliable enterprise account differently from a chronically late one, and adjust terms and outreach accordingly.

- Protect cash flow stability in B2B. For recurring and usage-based models, predictable billing and proactive collections are how to improve cash flow stability in b2b, smoothing out the peaks and troughs that make planning hard.

- Review and refine quarterly. Building how to improve your cash flow management into a regular review keeps small problems from compounding.

These practices compound. For a structured framework, our guide to accounts receivable automation best practices and our walkthrough of account receivables optimization go deeper on building a repeatable system.

Cash flow metrics worth tracking

How an AR platform improves cash flow

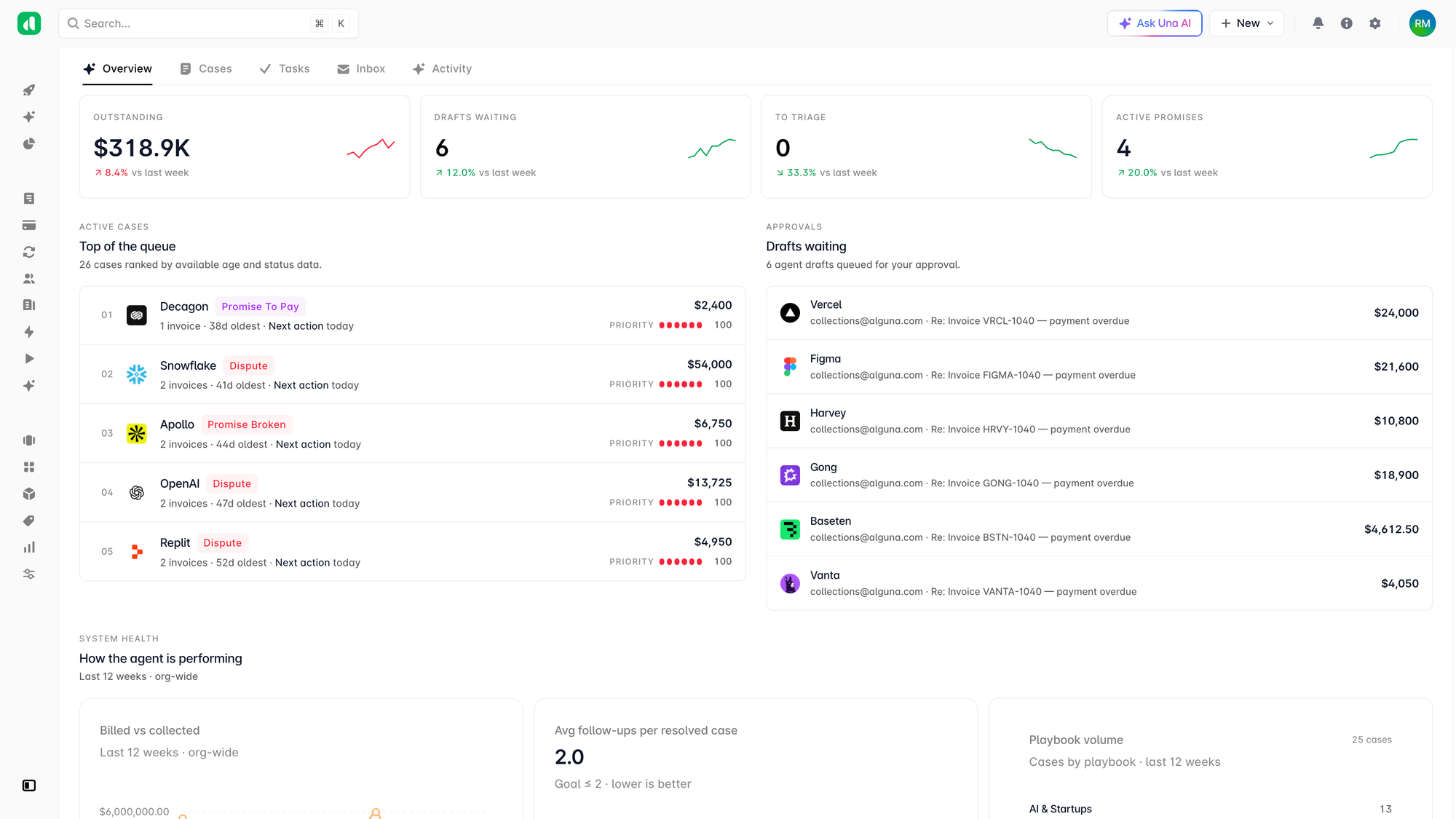

Most of the steps in this guide touch the same function: accounts receivable. That's why finance teams handling recurring and usage-based revenue increasingly turn to AI in accounts receivable to do the heavy lifting.

Alguna is built for exactly this, automating accounts receivable and B2B payments so the cash cycle tightens without adding headcount.

Here's how that maps to the cash flow levers above:

- Real-time visibility into what's owed. A live AR dashboard synced to your CRM and billing shows current, overdue, and at-risk invoices by customer segment or sales rep, which is the most direct answer to how to improve cash flow visibility.

- Automated collections and dunning. Reminders, smart retry attempts on failed payments, and escalation workflows run automatically, so overdue invoices keep moving without manual chasing.

- Multiple payment methods. Support for ACH, SEPA, wire, cards, wallets, and offline logging, with smart routing based on amount, region, and preferred currency, removes friction that delays payment.

- Auto-reconciliation. Payments match to invoices instantly and sync to QuickBooks, Xero, and your ERP, cutting month-end close effort and eliminating the manual errors that obscure your true cash position.

Because quoting, billing, and receivables live in one system, there's no data lag between when a deal closes and when an accurate invoice goes out, which is often where DSO quietly creeps up. The result is a shorter path from invoice to cash and a clearer view of cash flow at every step.

Improving cash flow is about improving processes

Improving cash flow isn't a single project with an end date. It's a set of habits: invoice quickly, set clear terms, automate the follow-up, make paying easy, watch your metrics, and keep a forecast in front of you.

Each one tightens the gap between the work you do and the cash you collect.

For B2B finance teams, the fastest and most controllable lever is accounts receivable. Get collections, payments, and reconciliation working together, and the rest of your cash flow becomes far easier to predict and manage.

Start with the step that addresses your biggest leak, then build from there.