Fintech billing sounds simple until you zoom in.

You're not just sending invoices. You're translating money movement into pricing logic, compliance-grade records, and revenue reporting. Often in real time. Across currencies. With refunds, disputes, FX, interchange, partner payouts, and strict audit trails.

Meanwhile, the economics are tightening. Payments is still a fintech “superstar” category for investment, but the bar for operational rigor keeps rising. And regulators are increasingly focused on transparency and controls across the payments stack.

This article breaks down the most common fintech billing challenges, why they happen, and practical ways to design billing that scales.

Why fintech billing is harder than SaaS billing

While SaaS monetization is quickly changing, traditional SaaS billing used to include seat count × plan price, billed monthly, with predictable upgrades and downgrades.

Fintech billing, on the other hand, is typically driven by financial events:

- Card transactions and interchange categories

- Payouts and settlement timing

- FX conversions and fees

- Risk controls and compliance requirements

- Refunds, reversals, chargebacks, and disputes

- Partner splits, commissions, and processor fees

That creates three systemic problems:

- Your billable units are messy (transaction types vary, rates vary, exceptions are common)

- The source of truth is fragmented (ledger vs processor vs product events vs CRM)

- Accuracy is high-stakes (a “small” billing bug becomes a regulatory, reputational, and margin problem)

10 fintech billing challenges you will hit as you scale

1) Pricing tied to interchange and network rules is inherently complex

If you monetize via card volume, interchange is not one clean percentage. Rates vary by card type, region, MCC, authentication method, and more. That variability makes pricing, invoicing, and margin reporting harder than teams expect.

What breaks in practice

- Blended pricing hides margin leakage

- You cannot explain invoices cleanly to customers

- Finance cannot reconcile “what we charged” vs “what we paid”

What good looks like

- A pricing catalog that supports rule-based rates (not just flat fees)

- Line items that remain explainable (grouping and rollups without losing traceability)

2) Fees and regulations move, and your billing logic must adapt fast

In payments, fee dynamics can change due to competition and regulatory pressure. The UK Payment Systems Regulator has scrutinized Visa and Mastercard on transparency and fee increases, which creates downstream pressure on fintech pricing and billing models.

What breaks

- Product ships a new pricing scheme, finance cannot operationalize it

- Customers churn because bills feel unpredictable or “black box”

What good looks like

- Configurable pricing rules and effective-date versioning

- Audit trails on “which rules applied to which events”

3) Multi-currency is not just “convert and invoice”

Fintechs expand globally early, and multi-currency introduces:

- FX rate sources and timing differences

- Invoice currency vs settlement currency mismatches

- Realized vs unrealized FX gains/losses

What breaks

- Inconsistent revenue numbers between billing, GL, and treasury views

- Customer disputes when FX logic is unclear

What good looks like

- Explicit FX policy (rate source, timestamp, rounding)

- Storing original currency, converted currency, and rate metadata per event

4) Real-time usage meets delayed settlement

Fintech revenue often looks real time in-product, but settles later. That lag complicates:

- Revenue recognition timing

- Accruals

- Receivables and collections

- “What happened” explanations when money lands days later

What breaks

- Month-end close becomes a forensic exercise

- Teams rely on spreadsheets because systems do not agree

What good looks like

- Separation of usage calculation from settlement and payout accounting

- Automated reconciliation pipelines (processor files, bank statements, internal ledger)

5) Refunds, reversals, and disputes create “negative billing” edge cases

Refunds are rarely a simple negative of the original transaction:

- Partial refunds

- Disputes and chargebacks with fees

- Representment outcomes

- Timing differences across reporting periods

What breaks

- Incorrect credits

- Mismatched customer balances

- Revenue and fee reporting that does not tie out

What good looks like

- Event-linked adjustments (refund references original charge)

- A customer balance model that supports wallets/credits cleanly

6) Taxes and e-invoicing requirements keep expanding

Fintechs selling across borders run into VAT/GST, digital services rules, and in some regions, mandated e-invoicing frameworks that require specific invoice fields and controls.

What breaks

- Invoices rejected by customers or local requirements

- Tax and finance teams forced into manual workarounds

What good looks like

- Tax-aware invoicing and jurisdictional configurability

- Invoice validation rules before anything is issued to a customer

7) Compliance expectations spill into billing systems

Even if billing is not your “compliance product,” regulators and auditors care about the integrity of money-related records. Public examples of fintech compliance gaps often come down to controls and monitoring not keeping pace with growth.

What breaks

- Weak audit trails on pricing changes

- Insufficient controls on approvals, write-offs, and adjustments

What good looks like

- Role-based permissions, approvals, and immutable logs

- Clear separation of duties between “configure pricing” and “approve financial impact”

8) Revenue recognition is harder with hybrid models

Fintechs increasingly bundle:

- Platform fees

- Usage or transaction fees

- Minimum commitments

- Tiered rates

- Partner revenue shares

That mix makes revenue recognition and contract modifications more complex, especially when pricing changes mid-term.

What breaks

- Deferred revenue schedules maintained manually

- Inconsistent treatment of amendments, credits, and true-ups

What good looks like

- Contract terms represented as structured data (not just PDFs)

- Automated schedules tied to the same events used for invoicing

9) Partner payouts and revenue splits add another ledger

If you support resellers, embedded finance partners, ISO programs, or affiliate deals, you now bill and pay out.

What breaks

- Disputes over commissions

- Inaccurate partner statements

- Margin unknown until weeks later

What good looks like

- A single event stream powering customer invoices and partner statements

- Configurable split rules and payout schedules

10) Billing data is scattered across too many systems

Many fintechs end up with:

- Product events in one place

- Processor data elsewhere

- CRM quote terms in another tool

- Invoices in a billing system

- Accounting in the GL

What breaks

- “Truth fights” during close

- Slow pricing iteration because every change is a migration project

What good looks like

- One canonical revenue event model

- APIs and workflows that unify quoting, billing, usage, and accounting sync

A practical blueprint for fixing fintech billing

If you want a billing stack that survives growth, aim for these principles:

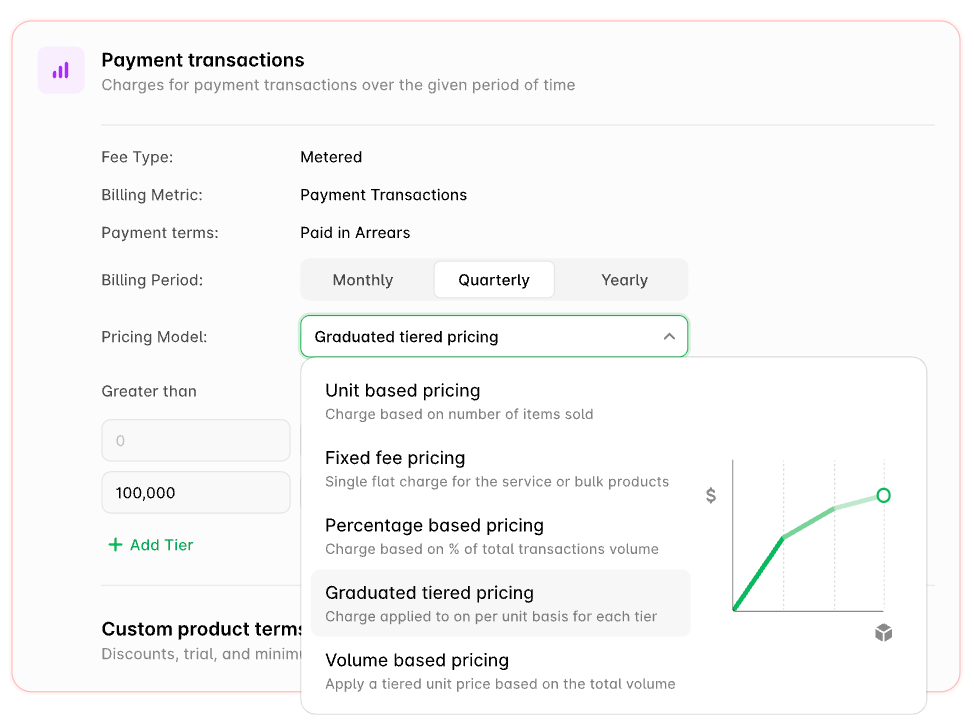

- Event-native metering: Capture and version billable events with rich metadata

- Rule-based pricing: Fees calculated by configurable logic (tiers, caps, floors, interchange-style variability)

- Explainable invoices: Rollups for readability, drill-down for trust

- Controls + auditability: Approvals, permissions, immutable logs

- Reconciliation built-in: Processor files + ledger + bank settlement tie-outs

- Multi-currency correctness: Rate source, timing, rounding, and stored FX context

- Contract-aware revenue: Structured terms that drive both invoicing and revenue schedules

Where modern fintech billing platforms fit in

Most teams hit a wall when they try to bolt fintech complexity onto “basic subscription billing.”

That is usually the moment to move to a quote-to-cash software that can handle:

- Custom pricing logic (including transaction-based and hybrid)

- Multi-entity and multi-currency invoicing

- Approvals and audit trails

- Automated accounting outputs and reconciliation support

Alguna: Pricing and billing platform built for fintech complexity

Alguna is a modern quote-to-revenue platform designed for fintech pricing and billing models that don't fit neatly into legacy subscription tooling.

Instead of forcing your team to stitch together a CPQ tool, a usage meter, a billing engine, and spreadsheets, Alguna centralizes the logic and data needed to monetize financial event streams accurately.

Fintech teams typically adopt Alguna when they need to support:

- Flexible and complex pricing models: Platform fees, per-transaction pricing, interchange++ or blended rates, tiered and volume discounts, minimum commitments, and hybrid plans.

- Custom contract terms: Ramps, trials, mid-term changes, proration, effective dates, and approvals that finance can trust.

- Multi-currency and multi-entity billing: Consolidated invoicing, local currency presentation, and clean reporting across entities.

- Metering and real-time event ingestion: A consistent event model that powers invoicing, customer reporting, and downstream accounting.

- Revenue-grade data: Structured terms and billing outputs that reduce month-end reconciliation and speed up close.

The practical benefit is simple: you can ship pricing changes faster, reduce manual reconciliation, and generate invoices customers actually understand, without sacrificing auditability.

Quick self-assessment: Are you at risk?

If you answer “yes” to 3 or more, your billing will likely become a growth bottleneck:

- We cannot clearly explain a customer’s invoice line-by-line.

- We cannot reliably reconcile billed revenue to processor or settlement data.

- Pricing changes require engineering work and backfills.

- Refunds and disputes routinely break reporting.

- Multi-currency causes close delays.

- Approvals and audit trails are inconsistent.

- Partner payouts are managed in spreadsheets.

If you checked “yes” to three or more, your billing is already costing you growth. The tax is not just extra finance hours. It shows up as slower pricing iteration, longer enterprise sales cycles, more invoice disputes, and ugly surprises at month-end close.

Removing challenges for good

The fixing the challenges in fintech billing doesn't come down to adding another spreadsheet or a one-off data patch. It's designing billing as a reliable system that can handle fintech reality: event-driven usage, variable fee logic, multi-currency settlement, refunds and disputes, and partner economics, all with auditability baked in.

Start with the highest-friction failure mode you have today, usually invoice explainability or reconciliation. Then move upstream: standardize your revenue event model, version your pricing rules, and automate the handoff to accounting and reporting.

Once those foundations are in place, you can launch new pricing and partner programs without turning every change into an engineering project.